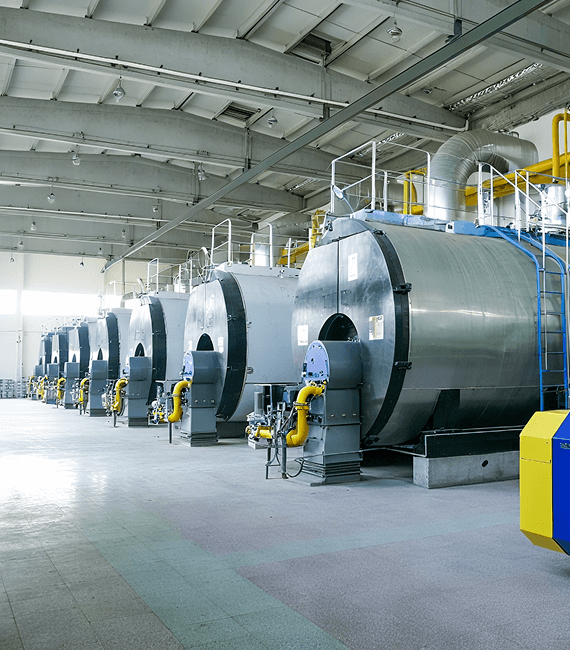

Circulating fluidized bed boilers, commonly referred to as CFB boilers, are thermal energy devices based on fluidized combustion technology. Compared to traditional boilers, their core advantages lie in three key areas: superior emissions control, broad fuel adaptability, and a wide load regulation range.

With the global emphasis on energy management, clean combustion has become a mandatory requirement across all industries. Traditional boilers are either limited to a single fuel type or struggle to meet emission standards, whereas CFB boilers effectively address these pain points—a key reason for their growing adoption by businesses.

When selecting a boiler, many companies prioritize environmental compliance and operating costs. CFB boilers meet stringent environmental standards without the need for additional complex desulfurization and denitrification equipment. At the same time, they can burn a variety of low-quality fuels, resulting in significant long-term cost savings—a key factor driving their gradual replacement of traditional boilers.

Translated with DeepL.com (free version)According to a report by Data Bridge Market Research, the global CFB boiler market was valued at US$525 million in 2021. Historical data indicates that this market has maintained a trajectory of steady growth, free from major fluctuations.

By 2029, the global market size is projected to reach US$1,046.1 million, reflecting a Compound Annual Growth Rate (CAGR) of 9.00% during the 2022–2029 period. This growth rate is considered quite substantial within the thermal energy equipment sector.

Numerous factors are driving this market expansion, with cost-effectiveness standing out as a particularly significant driver. Compared to traditional boilers, CFB boilers entail relatively lower upfront investment and subsequent operating costs, making them particularly well-suited for large-scale industrial applications.

The rising demand for clean energy has also provided a significant boost to the CFB boiler market. Moreover, the rapid expansion of the global oil and gas industry—which has increased the overall demand for thermal energy equipment—has further stimulated market demand for CFB boilers. This market report encompasses a wealth of practical information, including technological advancements, regulatory frameworks, PESTEL analysis, Porter's Five Forces analysis, supply chain analysis, raw material costs, and pricing analysis, thereby providing enterprises and investors with a comprehensive market reference.

The CFB boiler market can be segmented along various dimensions, with each segment exhibiting its own distinct developmental characteristics; understanding these specific market segments enables enterprises to identify their market positioning with greater precision.

Based on product type, the market is primarily categorized into three classes: subcritical, supercritical, and ultra-supercritical. Subcritical CFB boilers feature mature technology and the widest scope of application, currently maintaining a dominant position within both the industrial and power generation sectors. Supercritical and ultra-supercritical CFB boilers, conversely, prioritize high efficiency and energy conservation; as environmental regulations become increasingly stringent, their application scenarios—particularly in large-scale power plant projects—are steadily expanding.

In terms of capacity, the market can be segmented into units of less than 100 MW, 100–200 MW, 200–300 MW, and over 300 MW. CFB boilers with capacities under 100 MW are predominantly utilized by small and medium-sized industrial enterprises to meet their process steam and heating requirements; units exceeding 300 MW, on the other hand, are primarily deployed in large-scale power stations to fulfill massive electricity supply mandates.

Regarding fuel type, the key advantage of CFB boilers lies in their fuel flexibility, as they are capable of combusting a wide variety of fuels—primarily coal, biomass, and various other combustible materials. While coal remains the predominant fuel source at present, the demand for biomass-fired CFB boilers is on the rise, driven by the growing promotion of biomass energy. These boilers are capable of efficiently combusting not only high-quality coal but also various low-grade fuels—such as high-ash coal, high-sulfur coal, petroleum coke, and tailings—sustaining stable combustion without the need for auxiliary fuels.

In terms of application sectors, the market is broadly divided into energy and power generation, industrial applications, and other miscellaneous fields. Among these, the energy and power generation sector constitutes the largest application market, while the industrial sector primarily utilizes CFB boilers to generate process heat for industries such as petrochemicals, metallurgy, and building materials; notably, the oil and gas industry represents one of the core application scenarios for CFB boilers.

The global CFB boiler market exhibits distinct regional distribution patterns, with varying market characteristics and growth drivers across different regions. The Asia-Pacific and North American regions currently garner the most significant attention.

The Asia-Pacific region currently dominates the global CFB boiler market, holding a leading position in terms of both market revenue and market share. This dominance is primarily attributed to favorable environmental and energy policies enacted by governments across the region, coupled with the immense energy demand generated by rapid industrialization. In populous nations such as China and India, robust infrastructure development and industrial expansion have created a surging demand for thermal energy and electricity, thereby directly stimulating market demand for CFB boilers.

North America, conversely, represents the fastest-growing market, projected to maintain a high growth trajectory throughout the 2022–2029 period. Enterprises and end-users in this region possess a high level of awareness regarding clean energy and demonstrate strong environmental consciousness. Consequently, the robust demand for low-emission, high-efficiency equipment—such as CFB boilers—is driving rapid market expansion.

Regions such as Europe, the Middle East and Africa, and South America—while currently possessing relatively smaller market sizes—nonetheless hold significant growth potential. The European market benefits from stringent environmental regulations, which are driving the gradual adoption of CFB boilers. In the Middle East and Africa, accelerating industrialization processes are fueling a continuous increase in demand for energy equipment. Meanwhile, market growth in South America is primarily driven by investments within the energy and power generation sectors.

Furthermore, regional regulatory policies, trade tariffs, and local competitive landscapes also exert influence on the market positioning of CFB boilers. For instance, tariff policies in certain regions can impact the cost of imported CFB boilers, thereby altering the competitive dynamics within the local market.

The evolution of the CFB boiler market is shaped by a confluence of factors, encompassing drivers that propel market growth, challenges that constrain development, and numerous potential opportunities for expansion.

One of the core factors driving market growth is the high efficiency inherent in CFB boilers. These systems effectively reduce greenhouse gas emissions while simultaneously enhancing steam generation efficiency—attributes that make them particularly well-suited for applications within the coal-fired power generation sector. As global requirements for carbon emission reduction become more stringent, an increasing number of countries and regions are adopting Circulating Fluidized Bed (CFB) boilers to curb carbon emissions.

Demand from the oil and gas sector also serves as a significant driving force behind market growth. As a major consumer of electricity, the oil and gas industry generates the highest demand for CFB boiler installations; furthermore, the manufacturing and chemical sectors are also expected to gradually increase their utilization of CFB boilers in the future.

Additionally, the acceleration of global industrialization and urbanization, coupled with a growing awareness among enterprises regarding the inherent advantages of CFB boilers, is further contributing to the expansion of the market.

Growth opportunities are primarily driven by favorable government policies. To promote the development of green energy, governments worldwide have introduced various incentive measures—such as reducing the cost of components required for CFB boiler manufacturing—thereby providing substantial support for market development. For instance, regions such as Zhangzhou have enacted policies encouraging enterprises to procure and utilize highly efficient, energy-saving boiler equipment, thereby creating favorable conditions for the widespread adoption of CFB boilers.

In populous nations such as China and India, massive demand for infrastructure development and power generation—combined with rapid industrialization—has created a vast market landscape for CFB boilers.

The primary factor constraining market growth is the high overall cost involved. The installation costs for CFB boilers are relatively high, and subsequent maintenance requires significant investment; these factors, coupled with logistical and transportation challenges, often deter small and medium-sized enterprises (SMEs) from adopting the technology.

Driven by continuous technological iteration, the performance of CFB boilers is constantly improving, and their application scenarios are steadily expanding, with an increasing number of new technologies being integrated into actual industrial production processes.

Among the latest technological breakthroughs, the Low-Velocity Fluidization of Fine Gasification Residue (LFFF) CFB boiler stands out as particularly noteworthy. Jointly developed by Harbin Boiler Co., Ltd. and Tsinghua University, this technology is specifically designed for the disposal of fine gasification residue. It effectively resolves the complex challenge of achieving high-efficiency decarbonization of this residue, representing the world's first CFB boiler solution dedicated to the pure combustion of fine gasification residue—thereby filling a significant technological gap within the industry.

Fine gasification residue is a byproduct generated during the coal gasification process; in my country alone, the annual output exceeds 60 million tons. Traditional disposal methods are characterized by high costs and significant difficulties in achieving full resource utilization. The LFFF CFB boiler achieves the efficient utilization of fine gasification residue through combustion-based decarbonization. Compared to traditional processes, it offers greater simplicity and lower operating costs; it is currently slated for application in the National Energy Xinjiang Chemical Co.'s 240,000-ton/year fine gasification residue disposal project.

The core application fields for CFB boilers are extensive, encompassing waste treatment, oil and gas refining, power generation, and industrial heating. In the oil and gas sector, these boilers effectively process difficult-to-combust fuel byproducts—such as petroleum coke, heavy residues, and sludge—making them highly favored by oil refineries and petrochemical enterprises.

The advantage of fuel flexibility is clearly evident in practical applications. Beyond conventional fuels, CFB boilers can combust a diverse range of materials—including petroleum coke, biomass, refuse-derived fuel (RDF), and waste tires—thereby simultaneously reducing fuel costs and facilitating the resource-oriented utilization of waste. Furthermore, the fuel pretreatment system is remarkably simple; requiring a coal particle size of less than 10 mm, it eliminates the need for complex crushing equipment and is capable of directly combusting high-moisture coal with a water content exceeding 30%.

From a long-term perspective, the CFB boiler market is expected to maintain its growth trajectory. Between 2025 and 2031, the market size will continue to expand, while simultaneously giving rise to new development trends and challenges.

Long-term growth forecasts indicate that, driven by the continuous advancement of global clean energy policies, market demand for CFB boilers will experience further growth. This is particularly true in developing nations, where the acceleration of industrialization and infrastructure development will generate substantial additional market demand.

The resource-oriented utilization of solid waste is poised to become a pivotal development trend in the future. Industrial solid wastes—such as fine gasification residue—can be transformed into valuable resources through CFB boiler technology; this approach not only satisfies environmental protection mandates but also generates economic value, and such applications are expected to become increasingly widespread in the years to come.

Carbon footprint reduction and technological innovation will also serve as core drivers for market development. Enterprises will continuously optimize the performance of CFB boilers to reduce carbon emissions, enhance energy utilization efficiency, and introduce more competitive products. For instance, the 700 MW ultra-supercritical CFB boiler developed by Dongfang Boiler has, through technological innovation, successfully resolved the complex combustion challenges associated with high-altitude environments and high-moisture, low-calorific-value lignite, thereby achieving ultra-low emission standards. At the same time, the market faces several challenges that require resolution. CFB boilers involve a high degree of operational complexity and impose rigorous requirements on both operation and maintenance—factors that have limited their widespread adoption among small and medium-sized enterprises (SMEs). Optimizing costs and simplifying operational procedures—thereby enabling a broader range of enterprises to adopt CFB boiler technology—represents a collective challenge that the industry must address together.

Overall, the CFB boiler market holds promising prospects for future growth; whether viewed through the lens of expanding market scale or continuous technological innovation, it presents significant opportunities for both enterprises and investors.

Its core strengths lie in environmental compliance, fuel flexibility, and controllable costs, allowing it to align seamlessly with global trends in clean energy development while simultaneously meeting the practical operational needs of enterprises. For companies with substantial requirements for thermal energy and electricity, CFB boilers not only facilitate compliance with environmental standards but also yield long-term savings in operating costs.